Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

2026 Seattle & Eastside Farmers Markets

Wow, spring has sprung and 2026 is flying by…ready to renew your New Year’s resolution to eat better? Nothing makes it easier than a wide array of fresh, locally picked fruits and veggies. Add in some live music, amazing street food, and that feel-good knowledge that you’re supporting small businesses, and it’s a recipe for a great time. Here are all of the details so you can find a market near you or explore somewhere new…

Seattle Metro

- Ballard

- Capitol Hill (Broadway)

- Central District (Madrona)

- Columbia City

- Fremont

- Lake City

- Lake Forest Park

- Madison Park

- Magnolia

- Phinney

- Pike Place

- Queen Anne

- Shoreline

- South Lake Union – Thursday Market

- South Lake Union – Saturday Market

- U-District

- Wallingford

- West Seattle

Greater Eastside

- Bellevue – Crossroads

- Bellevue – Downtown

- Carnation

- Duvall

- Issaquah

- Kirkland – Downtown

- Kirkland – Juanita

- Mercer Island

- North Bend

- Redmond

- Renton

- Sammamish

- Woodinville

Seattle Metro

Ballard

Seattle’s first year-round Farmers Market, selling produce exclusively from Washington state farmers along the historic cobblestone stretch of Ballard Ave.

Sundays, 9am – 2pm | Year-Round

5345 Ballard Ave NW | Seattle

sfmamarkets.com/visit-ballard-farmers-market/

Capitol Hill (Broadway)

Come for Sunday brunch from food vendors who source ingredients from local, WA state farms (many of whom you’ll also meet selling their wares at the market). Live music and street performers often make an appearance, too.

Sundays, 11am – 3pm | Year-Round

Tuesdays, 3pm – 7pm (June 2 – September 29, 2026)

E Barbara Bailey Way | Seattle

seattlefarmersmarkets.org/chfm

Central District (Formerly Madrona)

Located in one of Seattle’s most diverse neighborhoods, you’ll find artisan foods as well as seasonal produce from Washington state farmers, fishers, and ranchers.

Fridays, 3pm – 7pm | May 15 – Oct 30, 2026

MLK Way & E Union St | Seattle

sfmamarkets.com/central-district-farmers-market

Columbia City

With everything from freshly harvested Asian greens to Ethiopian eats, come check out the immense variety King County’s most diverse zip code has to offer. Bring your bounty to adjacent Columbia Park for a picnic.

Wednesdays, 3pm – 7pm | May 6 – Oct 28, 2026

37th Ave S & S Edmunds St | Seattle

seattlefarmersmarkets.org/ccfm

Fremont

Seattle’s largest weekly street market is set along the Fremont Canal, and you can find just about everything at this “hyper market”—an eclectic mix of a farmer’s market, flea market and artists’ alley. The brunch food is pretty epic, too!

Sundays, 10am – 4pm

March 29-October: 3401 Evanston Ave N | Seattle

Nov-March: 701 N Northlake Way | Seattle

fremontmarket.com

Lake City

This celebrated North End seasonal market offers unique finds grown and prepared by local farms and food artisans. Enjoy kids’ activities, too!

Thursdays, 3pm – 7pm | June 4 – Sept 24, 2026

Saturdays, 10am – 2pm | Oct 3 – Dec 19, 2026

NE 125th St & 28th Ave NE | Seattle

seattlefarmersmarkets.org/lcfm

Lake Forest Park

With an emphasis on fresh, locally grown food, this market is an epicurean’s delight. Browse hard cider, baked goods, preserves, meat, pasta, sauces, and prepared foods along with the locally harvested fruits and veggies. There is also one “Crafts Market” each summer featuring local artisans.

Sundays, 10am – 2pm | May 10 – Oct 18, 2026

17171 Bothell Way NE | Lake Forest Park

www.thirdplacecommons.org/farmers-market

Madison Park

Stretching right alongside the park with its bathhouse and swimming beach, you’ll find ample produce from Washington State farms as well as delectable hot food vendors.

Saturdays, 10am – 2pm | May 16 – Oct 17, 2026

E Madison St & 42nd Ave E | Seattle

www.sfmamarkets.com/madison-park-farmers-market

Magnolia

This popular Saturday market is nestled in the tree-lined Magnolia Village. In addition to seasonal fruits and veggies, you’ll find sweet & savory pies, fresh bread, flowers, and more!

Saturdays, 10am – 2pm | June 6 – Oct 10, 2026 + Nov 21 & Dec 5

W McGraw St & 33rd Ave W | Seattle

seattlefarmersmarkets.org/mfm

Phinney

A popular gathering spot for both the Phinney Ridge and Greenwood communities, this market is right next door to a playground and offers live music in addition to the great mix of fresh produce and prepared food.

Fridays, 3pm – 7pm | June 5 – Sept 25, 2026 + Harvest Market on Nov 20

6532 Phinney Ave N | Seattle

seattlefarmersmarkets.org/pfm

Pike Place

Produce on Pike extends the standard market with pop-up tents from local farmers along the north end of Pike Place. Of course, you can come enjoy the historic indoor market any time…make it a day with great restaurants, eateries and retail shops, too.

Produce on Pike Farmers Market:

Wednesdays, 3pm – 7pm | June 24 – Sept 9, 2026

Stewart Street & Pike Place | Seattle

pikeplacemarket.org/farmers-markets

Indoor Market:

Daily, 9am – 6pm (farm tables close at 4pm) | Year-Round (Closed Thanksgiving & Christmas)

Pike Place between Pine & Virginia St | Seattle

(206) 682-7453

pikeplacemarket.org

Queen Anne

Seattle’s only independent farmers market, offering food, chef demos, live music, and children’s activities.

Thursdays, 3pm – 7:30pm | May 28 – Oct 8, 2026

Spring Preview Market on Sat, May 9, 2026, 10am-3pm

Saturday Harvest Markets on Oct. 31 & Nov. 21, 10am-3pm

Queen Anne Ave N & W Crockett St | Seattle

qafm.org

Shoreline

Now located at the BikeLink Park & Ride (corner of 192nd & Aurora, across from Sky Nursery), this market offers kids’ programs and live music in addition to its fresh Washington produce, organic meats, bread, honey, and prepared foods.

Saturdays, 10am – 2pm | June 6 – Oct 31, 2026

18821 Aurora Ave N | Shoreline

shorelinefarmersmarket.org

South Lake Union – Mini Thursday Market

Affiliated with Pike Place Market, this small satellite market offers locally sourced veggies, fruits, flowers, honey, jam, and organic meats from the region’s finest farms.

Thursdays, 10am – 2pm | June 4 – Oct 29, 2026

426 Terry Avenue N | Seattle

pikeplacemarket.org/farmers-markets/

South Lake Union – Saturday Market

This year, the former maker’s market is evolving into a full blown farmers market complete with over 100 booths and Space Needle views.

Saturdays, 10am – 3pm | June 6 – Nov 21, 2026

2100 6th Ave | Seattle

slumarket.com

University District

Come visit Seattle’s largest and oldest farm/food only market, regularly recognized as one of the best farmers markets in the U.S.! With over 80 booths and hard-to-find ingredients, it’s a chef’s delight.

Saturdays, 9am – 2pm | Year-Round

University Way NE (the “Ave”) between 50th & 52nd | Seattle

seattlefarmersmarkets.org/udfm

Wallingford

Located in Meridian Park, you can shop with the whole fam and then enjoy a picnic or playtime at the award-winning playground.

Wednesdays, 3pm – 7pm | May 27 – Sept 30, 2026

4800 Meridian Ave N | Seattle

sfmamarkets.com/visit-wallingford-farmers-market/

West Seattle

A weekend destination for families across the area, this market is set in the vibrant West Seattle Junction and features 90+ vendors during the summertime peak. Great community atmosphere celebrating Washington grown food and ingredients.

Sundays, 10am – 2pm | Year-Round

California Ave SW & SW Alaska | Seattle

seattlefarmersmarkets.org/wsfm

Greater Eastside

Bellevue – Crossroads

East Bellevue’s market features fruits, veggies & dairy products from Washington state farms along with hand crafted bird houses, candles, dog accessories, herbal wellness products, and more. Don’t miss the tacos, Nepalese street food, and handmade ice cream sandwiches, too!

Tuesdays, 12pm – 6pm | June 2 – Sept 29, 2026

15600 NE 8th St | Bellevue

https://crossroadsbellevue.com/music-events/crossroads-farmers-market/

Bellevue – Downtown

Set in the heart of Downtown Bellevue, this market offers goods exclusively produced within Washington state—from seasonal fruits & veggies to flowers, fresh meats, artisan goods, and prepared cuisine. The Power of Produce (POP) club empowers kids to know where their food comes from and make healthy eating choices.

Thursdays, 3pm – 7:30*pm | May 21 – Oct 1, 2026

*Closes at 7pm in Sept & Oct

Harvest Market: Nov 21, 10am – 3pm

1717 Bellevue Way NE | Bellevue

bellevuefarmersmarket.org

Carnation

Set in the heart of the Sno-Valley farming district, you’ll find plenty of freshly picked produce along with live music and educational activities for the kids.

Tuesdays, 3pm – 7pm | June, July & August 2026

Tolt-MacDonald Park, 31020 NE 40th St | Carnation

carnationfarmersmarket.org

Duvall

Nestled alongside the scenic Snoqualmie River, this friendly market features local eggs, jams, fresh roasted coffee, arts, crafts, and baked goods in addition to the seasonal veggies, fruits, and plant starts. Live music, picnic shelters and a playground make this a fun family destination.

Thursdays, 3pm – 7*pm | May 7 – October 8, 2026

*Closes at Sunset in October

Taylor Landing at 16201 Main St NE | Duvall

Parking Map

duvallfarmersmarket.org

Issaquah

Located at the historic Pickering Barn, this picturesque venue offers a variety of fresh farm and food-based products, concessions, and local artisans.

Saturdays, 9am – 2pm | May 2 – Sept 26, 2026 + Holiday Market Dec 12

Pickering Barn, 1730 10th Ave NW | Issaquah

Market Map

www.issaquahwa.gov/778/Farmers-Market

Kirkland – Downtown

This stunning setting on the Lake Washington shoreline turns shopping into a day at the beach. Peruse local produce and goods, then go for a swim or stroll along Moss Bay. Perfect for a picnic, too!

Wednesdays, 3pm – 7pm | June 3 – September 30, 2026

Marina Park, 25 Lakeshore Plaza | Kirkland

kirklandmarket.org

Kirkland – Juanita

Set in beautiful Juanita Beach Park on Lake Washington, you’ll find as many as 30 vendors offering farm fresh local produce, herbs, honey, nuts, flowers, plants, baked good, handcrafted items, and prepared cuisine. Make it a date with live music and a picnic at the beach. There’s a great playground for the kids, too.

Fridays, 3pm – 7pm | June 5 – Sept 25, 2026 (Closed June 19 & July 3)

Juanita Beach Park, 9703 NE Juanita Dr | Kirkland

www.kirklandwa.gov

Mercer Island

Come on down for quality local Washington state produce, cheese, fish, meat, bread, and more. Check out the live music schedule, too!

Sundays, 10am – 2pm | May 31 – Oct 11, 2026

Mercerdale Park, 7700 SE 32nd St | Mercer Island

www.mifarmersmarket.org

North Bend

This relaxed market enjoys live music and a spectacular Mount Si view. Vendors offer fresh produce, berries, honey, flowers, baked goods, hand-crafted items, and delicious prepared foods. Kids can participate in the Power of Produce (PoP) Club. Two playgrounds plus play fields and a covered picnic shelter make this a fun hangout spot. Leashed pets are welcome, too!

Thursdays, 4-8*pm | June 4 – Sept 3, 2026

*3:30 pm – 7:30 pm on Aug 27 & Sept 3

Si View Park, 400 SE Orchard Dr | North Bend

www.siviewpark.org/farmers-market.phtml

Redmond

Going strong since 1976, the Redmond Saturday Market offers a huge selection of vendors and dazzling array of produce, flowers, cheeses, preserves, salmon, tea, and handmade goods such as pottery and soaps. You’ll love the ready-to-eat foods, too.

Saturdays, 9am – 2pm | May 2 – Oct 31, 2026 (Closed May 9th)

9900 Willows Rd NE | Redmond

www.redmondsaturdaymarket.org

Renton

Find exclusively Washington-produced fruits, veggies, handmade goods, arts, crafts and more right in the heart of downtown Renton. Food trucks, live music, and kids’ activities make this a fun spot to liven up your Tuesday. Note: for 2026, the market returns to Piazza Park!

Tuesdays, 3pm – 7pm | June 2 – Sept 29, 2026

Piazza Park at 233 Burnett Ave S | Renton

www.rentonfarmersmarket.com

Sammamish

Each Wednesday, the Sammamish Commons plays host to a variety of local farmers, nurseries, bakeries, artisans, food vendors, and more. Live music and kids’ activities, too! Check out their special themed days including Soccer Fest and Pride Day.

Wednesdays, 4-8*pm | May 6 – Sept 9, 2026

*3-7 pm in Sept

Sammamish Commons, 801 228 Ave SE | Sammamish

Parking: Mary, Queen of Peace Catholic Church, 1121 228th Ave SE

www.sammamishfarmersmarket.org

Woodinville

Come check out downtown Woodinville’s Schoolhouse District and find produce grown in the state of Washington (and picked fresh for that morning!). You’ll also have an array of boutique baked goods, sauces, cider, artisans, and more to peruse.

Saturdays, 10am – 2pm | May 2 – Sept 26, 2026

13205 NE 175th St | Woodinville

woodinvillefarmersmarket.com

Find a Home | Sell Your Home | Property Research

Neighborhoods | Market Reports | Our Team

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

2737 77th Ave SE, Mercer Island, WA 98040 | (206) 232-0446

mercerisland@windermere.com

© Copyright 2026, Windermere Real Estate/Mercer Island.

How’s the Market? Q1 2026 Review of Seattle Area Real Estate

Across the region, median sales prices were lower than we saw at this time last year. The likely cause: more homes are hitting the market, but buyers (rattled by rising rates, layoffs, and an uncertain economy) aren’t keeping pace. That being said, we are still seeing many homes sell in their first 10 days on market with the choicest homes drawing multiple offers and selling above the asking price. The market is complex and every home is different…as agents, we have to look beyond the averages to get a clearer understanding of what is happening at the neighborhood level.

Despite the push in interest rates, it continues to be a good time to invest and find the right home! Buyers who are up-sizing have a special advantage when prices dip since the money they save on their purchase often exceeds the lower ROI from their sale.

Click or scroll down to find your area report:

Seattle | Eastside | Mercer Island | Condos | Waterfront

SEATTLE

When you look past the overall data, Seattle real estate is firing on all cylinders. Even though the median price is down YOY from $958,000 in 2025 to today’s $920,000 the actual median price point is hot, in city. We’re hearing tales of multiple offers in the $800,000-$1,200,000 price range from all corners of the core Seattle neighborhoods. 67% of homes sold for at or above list price, those that sold above sold for 104% (median) over list! The entire market average list to sales price is 101%, which bodes well for gains YOY in Q2.

West Seattle and Madison Park seem to be carrying the market, the only two neighborhoods to post stable or even a modest gain in price. Maybe not so ironically, Shoreline and Lake Forest Park saw among the highest gain in overall sales volume but also the biggest losses in median price at 10%. Shoppers are savvy and know when they’ve found a deal.

While our market is facing existential pressure from things like rising interest rates, war, and talks of recession; the city hasn’t looked this beautiful in years as officials prepare for World Cup festivities in a few months. There is always a bright side, and homebuyers appear to be seeing the silver lining as they consider their long-term investment plans. If you’ve thought about selling your home in 2026, we think this could be a great year: sales are happening, 55% within the first 10 days.

Click here for the full report and neighborhood-by-neighborhood statistics!

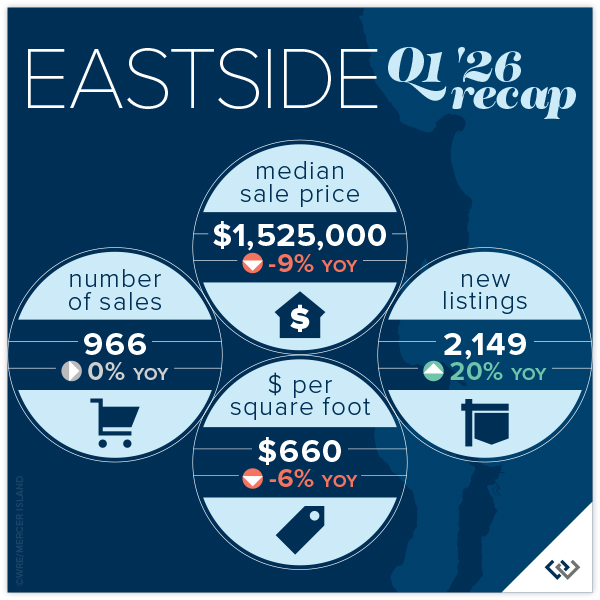

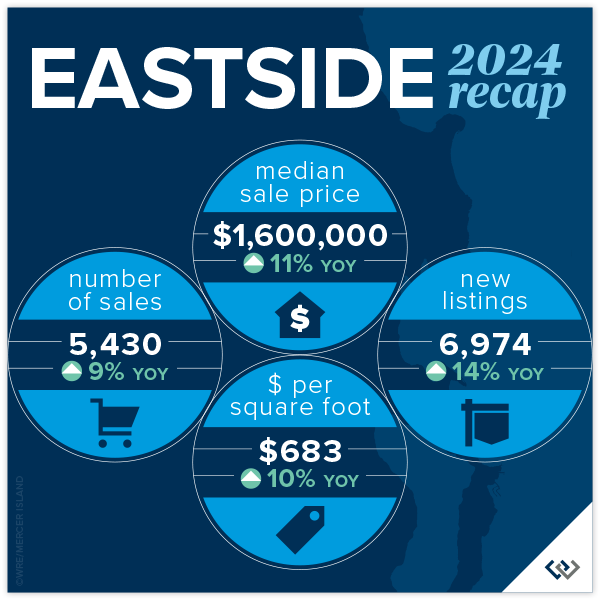

EASTSIDE

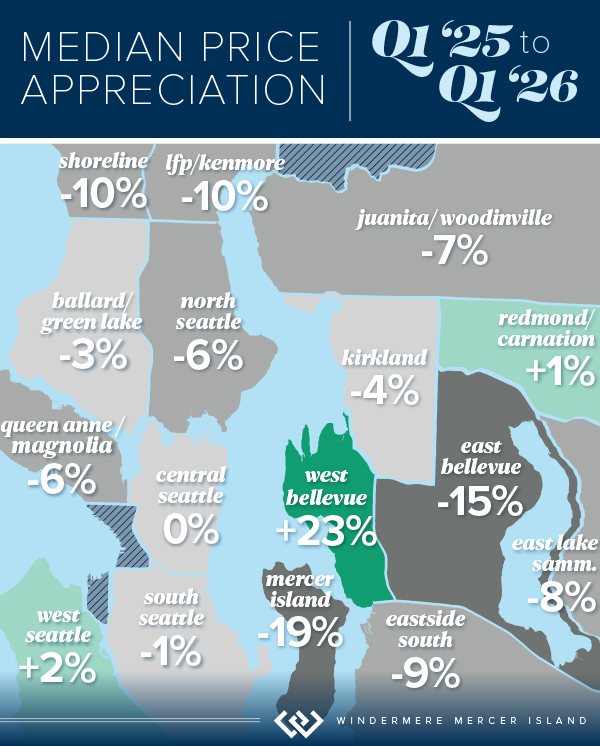

While median prices across the Eastside fell from $1,678,000 in Q1 2025 to $1,520,000, this quarter there are still bright spots. Namely, West Bellevue whose median price jumped 23% YOY. Though while the total number of sales were up in nearly every Eastside city, West Bellevue’s 36% dip drug the market down to report flat total sales: 966 at the end of Q1 2026 compared to 969 in the same period last year.

Mercer Island reported a region-wide high gain in average price per square foot at 14%, and West Bellevue was not far behind at 2%. All other neighborhoods had dips, topped by Redmond which fell 10%.

New listings rose 20% YOY, and this could mean many things but we think the two most likely are: home sellers got a head start in 2026 (we predict fewer new listings in Q2 than last year when new inventory nearly doubled from one quarter to the next) OR everyone else is as bullish about the market as we are. List to sales price ratios are at 99% on average and 51% of homes sold in the first 10 days. If you find the right home, don’t be afraid to jump.

Click here for the full report and neighborhood-by-neighborhood statistics!

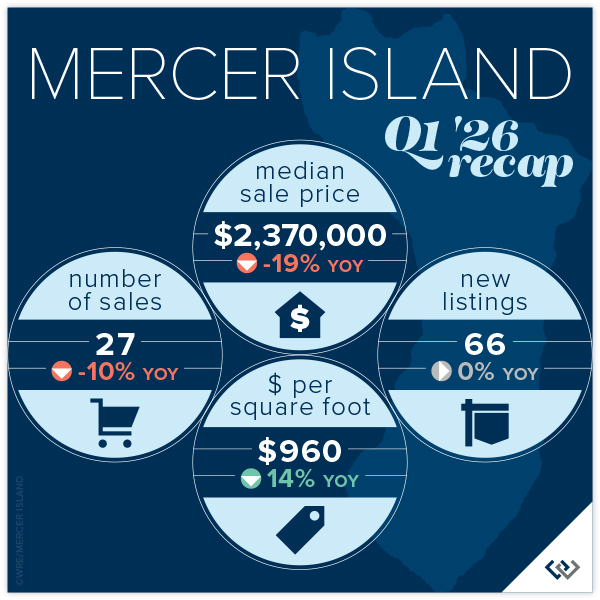

MERCER ISLAND

Island real estate seems to be off to a slow start in 2026 with median prices slipping YOY from $2,937,000 in 2025 to $2,370,000 in 2026. This is likely due to a spike in the months of inventory: 4.7 up from 2.9 last Q1. The months of inventory is a barometer for which way prices trend. High inventory = falling prices, supply/demand. That said, 60% of all homes sold for at or above list price and 63% sold in the first 10 days. Both of these numbers are indicators that homeowners are pricing to sell.

The condo market appears to be healthy this spring. Even though there are only 8 total sales that number is up a whopping 60% YOY. Median price is down 33%, but this is a rounding error with only 8 data points this year and 5 last year. A better indicator of market health is a 2.2 months supply of inventory, which is outpacing pretty much any segment of the market!

While our market is facing existential pressure from things like rising interest rates, war, and talks of recession; Mercer Island is now the “Bridge” in a whole new way with light rail open from Seattle to the Eastside. It will be interesting to see how this fun change affects the market as a whole.

Click here for the full report and neighborhood-by-neighborhood statistics!

CONDOS – SEATTLE & EASTSIDE

Seattle condo sales are up 8% over Q4 2025, an incredible seasonal boost. Though, the median price is down 6% YOY to $596,000. 25% of listed condos sold in the first 10 days and 48% of all condos sold for at or above list price. This tells us that agents and homeowners are tuned in to what a homebuyer in today’s market expects.

On the Eastside it’s a very similar story. Inventory is at 5.1 months. Meaning: at the current pace of sales, if no new listings came on the market, it would take nearly half a year to sell through the current inventory. That’s the highest since before 2020, the six year low was Q4 of 2021. Prices seem to reflect this, with an 11% dip in median home price down to $655,000 from Q1 2025: $740,000.

If you’ve thought about selling your condo in 2026, prepare for a highly saturated market where you’ll need to whip your unit into tip-top shape and price competitively to attract buyers. Inventory is up a combined 5%, while sales are down 21%. This is a big gap that will definitely create downward pressure on pricing if the gap between demand and supply widens. If you have the luxury to wait and watch, that might be your best option. If you’ve thought about buying, this is an excellent year to consider your options. Just remember, if you find the right nest and it hasn’t been on the market long: jump in! The good ones don’t last.

Check out area-by-area details in the full condo report.

WATERFRONT

Seattle and the Eastside both had fewer waterfront sales this quarter than we saw in Q1 of 2025, whereas Lake Sammamish posted the same number of sales and Mercer Island saw a boost. The vast majority of homes sold at or below their listed prices with the exception of one mid-century Magnolia home on 75 feet of waterfront that garnered over $300k above and beyond its original asking price.

The highest sale was in Hunts Point at $17+ million for a stunningly reimagined English Tudor on 3/4-acre with extensive waterfront. The most modest sale was in Rainier Beach: an original 1980 home on 50 feet of waterfront that went for $1,640,000.

This brief overview of the entire Seattle-Eastside private waterfront market, including Mercer Island and Lake Sammamish, illustrates the trends occurring in our region over time. This data is interesting and insightful but cannot replace an in-depth waterfront analysis with your trusted professional.

View the full waterfront report

Find a Home | Sell Your Home | Property Research

Neighborhoods | Market Reports | Our Team

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

2737 77th Ave SE, Mercer Island, WA 98040 | (206) 232-0446

mercerisland@windermere.com

© Copyright 2026, Windermere Real Estate/Mercer Island. Information and statistics derived from Northwest Multiple Listing Service and Trendgraphix, and deemed accurate but not guaranteed.

Seattle report cover photo courtesy of The Sirianni Group; and Andrew Webb, Clarity NW Photography.

Eastside report cover photo courtesy of Tori Franzen; and Michael Tilzer Photography.

Mercer Island report cover photo courtesy of Julie Wilson; and Chris Neir, Clarity NW Photography.

Condo report cover photo courtesy of Marianne Parks; and Christopher Cooper, Clarity NW Photography.

Should You Sell Your Home Off-Market?

In today’s real estate market, sellers are often presented with different strategies for selling their homes. One of the most debated topics is whether to list a home on the open market or to sell it off-market through private channels. While there may be rare instances where an off-market sale makes sense, the reality is that exposing your home to the full market is the best way to ensure a fair, competitive, and profitable transaction.

The Risk of Fair Housing Issues in Off-Market Sales

Selling a home off-market can create unintended fair housing concerns. The Fair Housing Act exists to ensure that all buyers have an equal opportunity to purchase a home, regardless of race, religion, gender, familial status, or other protected characteristics. When a home is sold privately, the pool of potential buyers is inherently limited, which could lead to discriminatory practices—intentional or not. Open market listings ensure that every qualified buyer has the opportunity to compete, making the transaction transparent and equitable.

Competition Drives Higher Prices

One of the most compelling reasons to list on the open market is the power of competition. Real estate is fundamentally a supply-and-demand-driven industry, and competition among buyers is the most reliable way to achieve the highest possible sale price and favorable terms for a seller.

Consider recent data from metro King County: 30% of homes sold over the asking price. In Seattle, where the median home price is $945,000, those homes sold for a median of 4% over list price—translating to an additional $37,800 in a seller’s pocket. On the Eastside, where the median home price is $1,600,000, that number jumps to a 5% median premium, equating to an extra $80,000. These numbers illustrate the clear financial advantage of market exposure. The more buyers who see a home, the greater the likelihood of multiple offers, which naturally drives prices upward. Further, when buyers compete, they compete with strong terms not just on price. Things like faster closing, free rent back, earnest money delivered up front, can all be negotiated given the proper market exposure.

Why Do Some Buyers Want Off-Market Sales?

When a buyer is pushing for an off-market transaction, it’s worth questioning why. Often, buyers seeking off-market deals are looking to sidestep competition in order to secure a home for less than they’d pay in a bidding war. In some cases, they may even be investors looking to purchase a property below market value to maximize their own return. While these buyers may frame their offer as a benefit to the seller—offering convenience and a quick close—the reality is that they are often the primary beneficiaries of such transactions.

Are There Ever Valid Reasons to Sell Off-Market?

There are a few instances where an off-market sale may be appropriate. High-profile sellers who require discretion, homeowners dealing with sensitive personal circumstances, or those who have already pre-negotiated a deal with a trusted party may choose to sell privately. However, for the vast majority of sellers, the goal is to achieve the highest return with the smoothest transaction possible. That can only be accomplished with full market exposure.

Beware of Gimmicks Disguised as Benefits

Some firms may try to sell you on the idea that off-market sales are in your best interest. Be wary of these claims. Often, this is simply a tactic to get their foot in the door—to secure a listing without having to do the full marketing and exposure necessary to achieve the best result for you. If an agent is recommending an off-market sale, ask yourself who stands to benefit the most: you, them, or the buyer?

The Bottom Line: Listing on the Open Market Equals Maximum ROI

If your priority is securing the highest price and ensuring a fair and competitive process, listing your home on the open market is the clear choice. The numbers don’t lie—competition drives higher prices, and transparency ensures fairness. It’s so easy to get caught up in the whirlwind of an off-market offer. And it’s flattering to feel like your home is so appealing that people are knocking on your door before it even debuts. For some, the privacy of an off-market sale offsets the considerable dollars left on the table. But for most of us, those dollars matter. And having multiple interested buyers instead of just one means better terms and more certainty as you head towards the closing table. While off-market sales may have their place in very specific situations, they should not be embraced as a superior alternative. An experienced real estate professional will always prioritize your financial best interests over convenience-driven gimmicks.

Find a Home | Sell Your Home | Property Research

Neighborhoods | Market Reports | Our Team

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

2737 77th Ave SE, Mercer Island, WA 98040 | (206) 232-0446

mercerisland@windermere.com

© Copyright 2025, Windermere Real Estate/Mercer Island.

How’s the Market? Annual Review of Seattle Area Real Estate

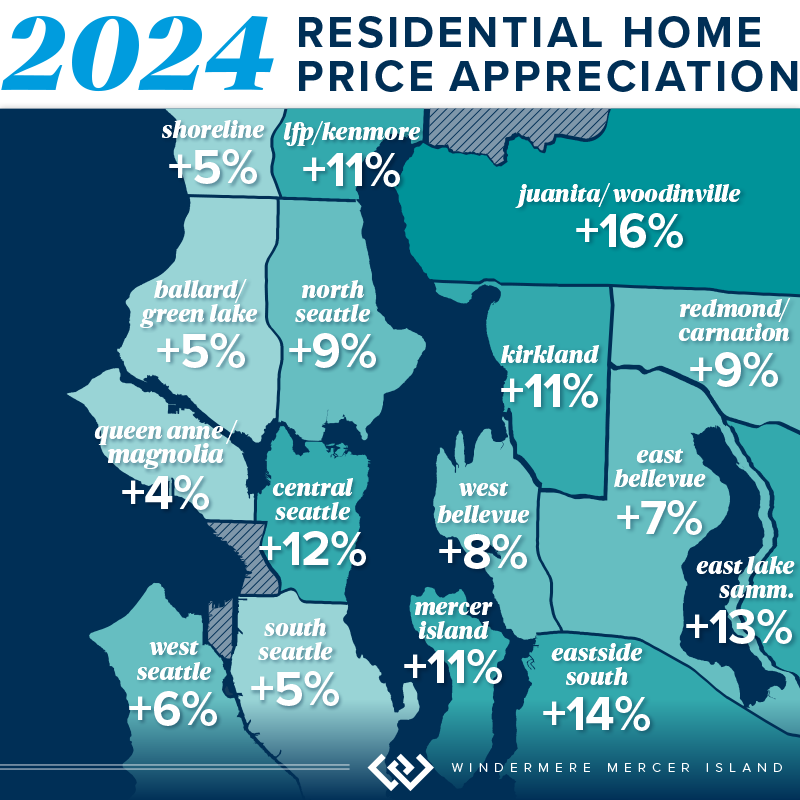

Happy New Year! Whew, we made it! With 2024 now in the books, we’re looking back fondly on a real estate market that showed positive signs of growth in virtually every sector. Median sales prices posted strong double-digit gains on the Eastside along with a healthy 8% rise in Seattle. Listings also rose, easing the strain for buyers grappling with our housing shortage.

If you’ve waited long enough and 2025 is the year for you to make a move, we recommend front loading that decision. Pent up demand (both sellers waiting to sell and buyers waiting to buy) should give us a spring full of blossoming and beautiful inventory. There is less volatility in interest rates than there has been in recent months, you’ll see that the average rate has been rock steady around 6.75% in 2023 and 2024. Overall, this is a great time to buy or sell and I know your real estate professional is excited to help you!

Click or scroll down to find your area report:

Seattle | Eastside | Mercer Island | Condos | Waterfront

SEATTLE

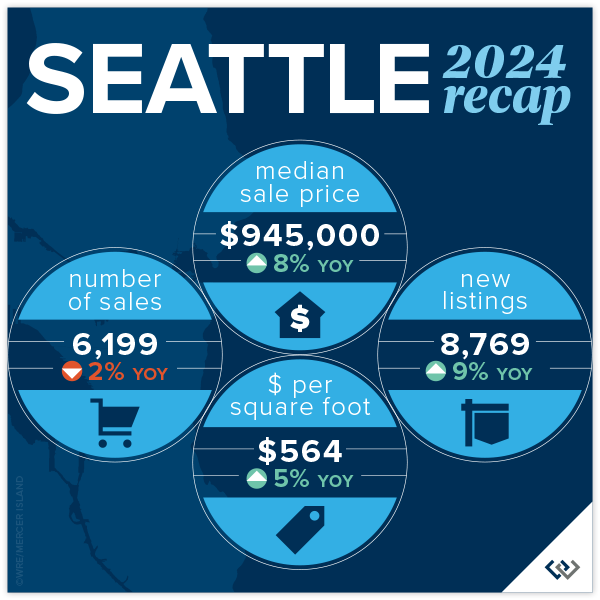

From a statistical/real estate perspective, the numbers don’t really reflect the overall vibe of the year. In a good way! It’s all positive news: prices are up, listings are up, and market time is down. The City of Seattle is in full recovery mode. Homeowners are awaiting the new density plan and eager to learn what the city has in store for the core neighborhoods around transit. It’s an exciting time. Median sold price city-wide reached a record $945,000 (modest, as that is $5000 above the previous record set in 2022) and homes sold for an average 104% of list price when they attracted a sale in the first 10 days (58% of the total sales).

Lake Forest Park and Madison Park saw the greatest price gains at 11% and 12% respectively. North Seattle was over all the “strongest” with 66% of homes selling in the first 10 days and 70% of homes selling for at or above list price. There was a modest gain in new listings across the board at 8769, while still lower than typical. The ten-year average is around 10,500 listings per year. No bad news here with average price per square foot gains of 5% to $564!

Click here for the full report and neighborhood-by-neighborhood statistics!

Click here for the full report and neighborhood-by-neighborhood statistics!

EASTSIDE

Welcome 2025! We (the real estate community) are feeling hopeful and bullish about what’s to come. So far, the numbers year over year support that. When we reviewed 2023 for the Eastside, the only positive statistic reported was Mercer Island’s 2% rise in the number of home sales. Looking at the 2024 report with that perspective it is ALL good news. New listings are up 14% for the year, while the number of sales are up nearly 10%. This is absorption of inventory to be excited about. Prices are up 11% to a record high of $1,600,000!

Woodinville and the area S of I-90 saw the largest price gains at 16% and 14% respectively, likely enjoying the benefits of buyers ‘pushing out’ because of the pressure of affordability in the core neighborhoods. Kirkland and West Bellevue were among the highest total sales and still a strong showing in price gains at 11% and 8%. Even though Bellevue (E of 405) saw the most modest price gains this was arguably the most popular neighborhood with 74% of homes selling in the first 10 days and 71% selling for at or above asking price!

Click here for the full report and neighborhood-by-neighborhood statistics!

Click here for the full report and neighborhood-by-neighborhood statistics!

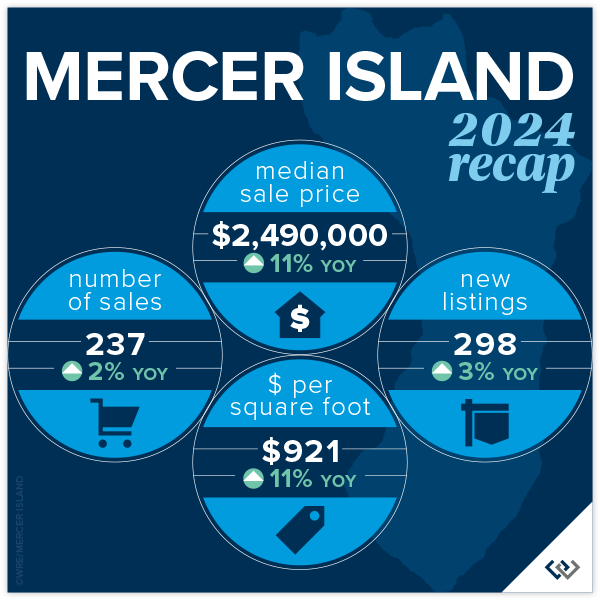

MERCER ISLAND

2024 was a solid year for Mercer Island: 11% overall price growth, on average 98% list to sales price ratio, and a respectable 32 cumulative days on market. This was a year of calm and confident decisions made by the entire real estate market. Home buyers and sellers alike. Looking to the neighborhoods there were two that stood out in relation to 2023: The Eastside and The Lakes where total sales had massive growth. 26 homeowners (vs 11 in 2023) moved on the Eastside and in the Lakes there were 4 transactions, a whopping change given that there were no sales reported on the MLS in 2023. The Island has not yet reached the peak prices from 2022, but we’re on our way!

Shifting to the condo market, 2024 was a sleepy year. With 47 new listings and 33 sales (both about 20% lower than in 2023), the average list to sales price ratio of 101% surprised us! Total median price is down YOY by about 8%, but with such little data to draw from this number tends to swing more than most. The overall price swing was from $339,000 for a studio to $1,775,000 for a 2 bedroom luxury unit. 19 of the 33 sales were 2 bedroom units. All in all condos on the island are a necessary market segment that we continue to watch closely as an overall indicator of market health.

Click here for the full report and neighborhood-by-neighborhood statistics!

Click here for the full report and neighborhood-by-neighborhood statistics!

CONDOS – SEATTLE & EASTSIDE

In reviewing last years’ report, there was so much RED! This year is a refreshing change with some positive numbers sprinkled in. Even the pockets that remain flat feel like good news, after all, a push is a win! Perspective is everything, in life and in real estate. This year was absolutely a bright spot for condos in the last several months. This was due in large part to external factors: affordability issues in single family, perceived ‘high’ interest rates, continued density issues in the ‘burbs, and major employers recall to office. Urban life in both Seattle and on the Eastside are experiencing a renaissance and we’re here for it!

The headline in Seattle is that prices are UP! Downtown saw an increase of 8% to a median price of $650,000. Though, North Seattle carried the day with an eye popping 18% increase in median price. While price per square foot was flat on average, new listings are up 21% YOY. Sellers are dipping their toes back in the market at higher prices (up 5.3%) and seeing moderate success with total sales down 3% (compared to a 26% drop in 2023). Buyers know they have options and will wait to pick off the low hanging fruit: best perceived value for their dollar.

Meanwhile, on the Eastside: prices are up, listings are up, sales are up. A nice headline, but let’s break it down. New listings rose a whopping 34% year over year (which you may remember saw a 23% dip from 2022). Demand was steady with total sales up 15% YOY; we didn’t quite absorb all of the new inventory but that is to be expected. So, even with a relatively high absorption rate prices rose to a record high median of $695,000. The stars of this price gain are, not surprisingly, Kirkland and West Bellevue at 28% and 24% respectively. We can’t wait to see what 2025 will bring!

Check out area-by-area details the full condo report.

WATERFRONT

The Eastside saw a huge boost in waterfront sales with 50% more sold in 2024 than 2023. Mercer Island and Lake Sammamish posted similar sales gains of 45% and 43% respectively. While Seattle had 2 fewer sales than the year prior, its waterfront homes sold faster than in any other area and fetched higher selling prices as compared to list prices.

The highest waterfront sale was $38,900,000 for an immense 13,590 sq. ft. Medina estate on 117 feet of Lake Washington shoreline. The most modest sale was $1,400,000 for a 1960 Ralph Anderson original on Seattle’s Arroyo Beach.

This brief overview of the entire Seattle-Eastside private waterfront market, including Mercer Island and Lake Sammamish, illustrates the trends occurring in our region over time. This data is interesting and insightful but cannot replace an in-depth waterfront analysis with your trusted professional.

Find a Home | Sell Your Home | Property Research

Neighborhoods | Market Reports | Our Team

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

2737 77th Ave SE, Mercer Island, WA 98040 | (206) 232-0446

mercerisland@windermere.com

© Copyright 2025, Windermere Real Estate/Mercer Island. Information and statistics derived from Northwest Multiple Listing Service and Trendgraphix, and deemed accurate but not guaranteed. Seattle cover photo courtesy of Michael Fleming and Clarity Northwest Photography. Mercer Island cover photo courtesy of The Sirianni Group and Clarity Northwest Photography. Condo cover photo courtesy of Luke Bartlett and Matthew Gallant, Clarity Northwest Photography.

How’s the Market? Q3 2024 Review of Seattle Area Real Estate

While Q3’s summertime market slowed a bit from the frenetic spring pace of Q2 (we call this the “Summer Slump”), median home values are up across the region compared to this time last year. Most homes still sold at or above their listed prices in the first 10 days on market. However, buyers had more choice with higher inventory levels AND some room to negotiate on price for those homes that stayed on the market past the 10-day mark.

What does this mean for the rest of 2024? We typically see buyer activity decrease as we head into the holidays, and of course, it’s also election season. If you’ve been considering a purchase and are of the mindset that you don’t want to compete, THIS IS YOUR MARKET! For sellers the average days on market in Q3 was 20 for Seattle and 18 for the Eastside. Which means: if your price didn’t attract a buyer in the first two weeks, it’s probably time to re-evaluate. Interest rates are better than they’ve been since mid 2022. Quality inventory is being presented to the market. If you see a great house, be prepared to move quickly. Opportunity Knocks.

Click or scroll down to find your area report:

Seattle | Eastside | Mercer Island | Condos | Waterfront

SEATTLE

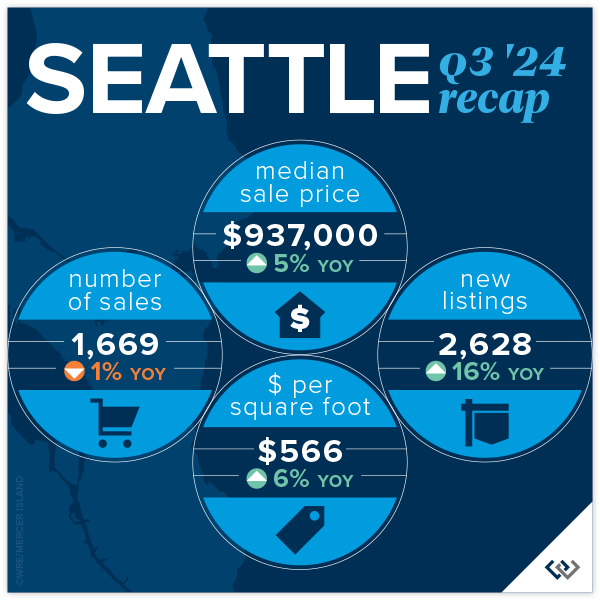

Lots of good news in Seattle during our post-summer glow. Prices are up year over year by 5% to $937,000. While we’re still under the peak median of $1,000,000 set in Q2 of 2022 and $970,000 from last quarter, this is so typical for Q3. We’ve seen it every year from Q2 to Q3 going back to 2018 (except in 2020 largely because the real estate market shut down completely in Q2). Buyers had lots of choice, with more inventory to end the quarter than we’ve had since Q3 of 2022. Even with these buyer bright spots we still saw 56% of homes sell in the first 10 days and 34% over the asking price.

Average price per square foot and median price were in positive territory across the board this quarter in all neighborhoods. Richmond Beach/Shoreline and Madison Park/Capitol Hill both saw larger than typical gains in $/sq.ft. (11%) and median price (10%) respectively. North Seattle appeared to be the “hottest” market around with 64% of homes selling in the first 10 days. Again, really great numbers in Seattle given that Summer Slump was in full effect.

Click here for the full report and neighborhood-by-neighborhood statistics!

Click here for the full report and neighborhood-by-neighborhood statistics!

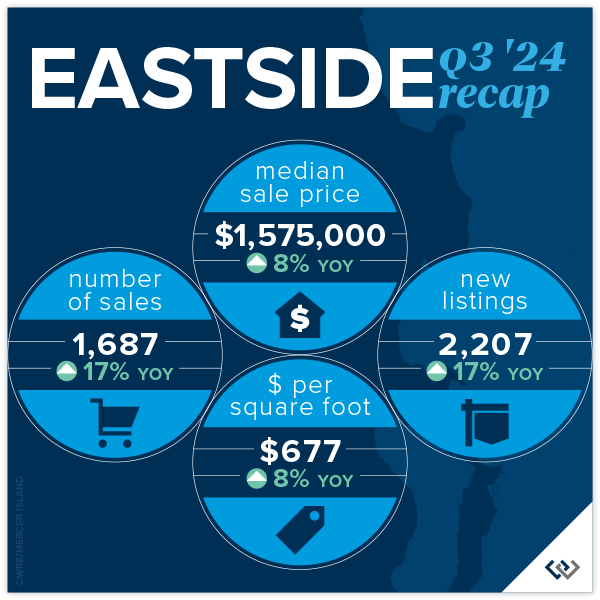

EASTSIDE

The Eastside continues to be the region’s crown jewel of real estate. Median prices are up again year over year by 8%. Most of us felt what we lovingly call the Summer Slump, and the numbers confirmed this. Prices (median) AND transactions were down 6% overall when compared against Q2 of 2024. That’s a $100,000 dip in median sales price if you missed the spring market. This is absolutely typical for the PNW and Metro King County. Seasonally our peak seasons are spring and post Labor Day/pre-holiday. This year that may be disrupted by election distractions. Time will tell if it’s a market lacking in consumer confidence or simply existential distraction.

The micro markets across the Eastside are fairly homogeneous. Among the 8 neighborhoods that we track, the median price swing was 3-11% but all in a positive direction. Total transaction volume is up 18% signaling that eventually life changes will trump a 2.5% interest rate. While homes were mostly selling in the first 10 days, multiple offers/paying over asking price were not the norm. In fact, the split between at, above, and below was relatively even.

Click here for the full report and neighborhood-by-neighborhood statistics!

Click here for the full report and neighborhood-by-neighborhood statistics!

MERCER ISLAND

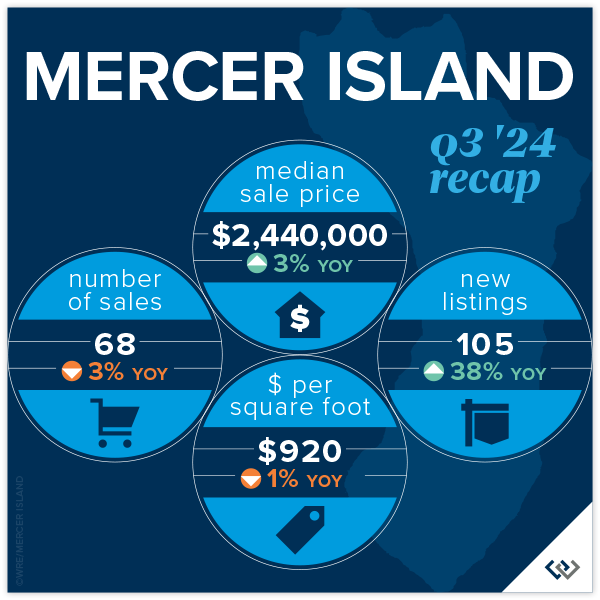

Fall has come for Mercer Island. The summer construction on Island Crest is done, school buses are out en force, and those filtered views that only come out in winter are starting to show. It’s time to look back fondly at the summer real estate market: prices are up YOY by 3% to $2,440,000 to end the quarter. This is likely more about trailing gains from a robust spring than it is about actual gains from Q3, given the indicators. A whopping 40% of homes sold under list price. It took 40% longer than 10 days to sell (not necessarily the same 40%) but only for about a 2% discount. This suggests that seller pricing and buyer motivation are evenly matched. There were 50 active listings at end of quarter, the most since Q2 of 2020 when real estate shut down completely.

Focusing on neighborhoods, The Lakes, Mercerwood, Mercerdale, and Mercer Island Estates saw 100% of homes sell in the first 10 days for an average of 102% of sales price. This goes to show that in any market, despite overall conditions, there will always be “hot homes.” Mid-Island had the most overall activity with 22 of the 68 sales across the Island. These occurred at $865/foot and 16 of the 22 homes sold in the first 10 days for at or above list price.

Click here for the full report and neighborhood-by-neighborhood statistics!

Click here for the full report and neighborhood-by-neighborhood statistics!

CONDOS – SEATTLE & EASTSIDE

Once again, we’re rooting for the Seattle condo market as it proves to be the little engine that could! Chugging along toward modest price gains even when the rest of the market seems to be struggling a bit, Seattle condo prices have held steady for the last 6 quarters, with mostly positive change. Eastside condos hit a median price all-time high in Q2 at $709,000. We’re off of that a touch to $690,000 in Q3, to be expected after a beautiful summer. The Eastside ended the quarter with 29% more listings than this time last year and only 13% more sales. Mounting inventory tends to lead to price softening. Overall, nearly 50% of condos sold for at or above their list price!

When you compare the charts in the report, there is admittedly more positive news on the Eastside than in Seattle. Overall, we’re encouraged that despite many neighborhoods experiencing a drop in sales, average price per sq. ft. held flat and median price is up overall. On the Eastside it’s still great news all around for the market, especially in West Bellevue with 26% median sales price gains and total sales up 55%.

Friendly PSA: PLEASE remember that there is a ‘first rung’ of the property ladder. CONDOS create an affordable option to start building wealth at a younger age. It’s an important real estate product that has been overlooked. I am hopeful that enterprising young homeowners return to the condo market in droves this next real estate cycle.

Check out area-by-area details the full condo report.

WATERFRONT

While a bit slower compared to last quarter, waterfront sales remained strong in Q3 with 10 on the Eastside and 8 in Seattle. Lake Sammamish moderated in summer with just 5 sales compared to the crazy 15 we saw in spring, while Mercer Island stayed fairly steady with 4 (compared to 6 in spring). The highest sale was nearly $18 million for an immense Wendell Lovett designed 6,920 sq. ft. home on 125 feet of prime “gold coast” waterfront in Medina. The most modest sale was also on the Eastside—an original 1943 cottage on 53 feet of west-facing waterfront in Kennydale.

This brief overview of the entire Seattle-Eastside private waterfront market, including Mercer Island and Lake Sammamish, illustrates the trends occurring in our region over time. This data is interesting and insightful but cannot replace an in-depth waterfront analysis with your trusted professional.

Find a Home | Sell Your Home | Property Research

Neighborhoods | Market Reports | Our Team

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

2737 77th Ave SE, Mercer Island, WA 98040 | (206) 232-0446

mercerisland@windermere.com

© Copyright 2024, Windermere Real Estate/Mercer Island. Information and statistics derived from Northwest Multiple Listing Service and Trendgraphix, and deemed accurate but not guaranteed. Seattle cover photo courtesy of Kathryn Buchanan and Brandon Larson, Clarity Northwest Photography. Mercer Island cover photo courtesy of The Sirianni Group and Clarity Northwest Photography. Condo cover photo courtesy of Julie Wilson and Bobby Erdt, Clarity Northwest Photography. Waterfront cover photo courtesy of Anni Zilz and Andrew Webb, Clarity Northwest Photography.

Property Tax Relief Programs in King County

Updated 2/2025

More than 26,000 low-income seniors and disabled people in King County who qualify for a tax exemption haven’t claimed it…are you or your family member one of them?

If you are homeowner, make $84k or less per year, and are either age 61+, retired due to disability, or 57+ and the surviving spouse/domestic partner of an exemption participant, there is a good chance you qualify. You can even retroactively apply for the exemption for the prior 3 years!

Scroll down for details on this exemption plus 4 other property tax relief programs that King County offers.

In another county? Here is the full list of income thresholds for every county in Washington State, and here is another link to view the programs each county offers.

Senior/Disabled Property Tax Exemption

WHAT IS IT?

A reduction in King County property tax for seniors, people with disabilities, and disabled veterans.

WHO QUALIFIES?

- Seniors age 61+

or

- Those who cannot work due to a disability

or

- Veterans with service-related disabilities (evaluation of at least 80% or receiving compensation from the VA at the 100% rate)

or

- Those who are age 57+ AND a surviving spouse/domestic partner of an exemption participant who was enrolled at the time of their death

YOU MUST…

- Own your home

- Have occupied it as a primary residence at least 6 months out of the year

INCOME LIMIT

- $84,000 maximum annual household income for the previous year in King County (click here for other counties)

WAYS TO APPLY

- Click here to apply online

- Call 206-296-3920

- Ask your local senior center if they help with applications

Senior/Disabled Property Tax Deferral

WHAT IS IT?

The ability for seniors & disabled people to defer unpaid property tax/special assessments, including back taxes for as long as you’ve owned the home. Deferred taxes + any accumulated interest then become a lien on the property until it’s repaid.

WHO QUALIFIES?

- Seniors age 60+

or

- Those who cannot work due to a physical disability

YOU MUST…

- Own your home and have lived in it for more than 9 months in a calendar year

- Meet an equity requirement

INCOME LIMIT

- $88,998 maximum annual household disposable income in King County (click here for other counties)

HOW TO APPLY

- Call 206-263-2338

MORE TAX RELIEF PROGRAMS…

Limited Income Deferral

WHAT IS IT?

The ability to defer the second installment of your property taxes/special assessments (normally due October 31st) if you are a low-income homeowner. The deferred taxes plus interest become a lien on the property until they’re repaid.

YOU MUST…

- Have owned your property for 5 years

- Be living in the home as of January 1st of the application year AND more than 9 months during that year

- Meet an equity retirement

- Have already paid the first half of your taxes (due April 30th)

INCOME LIMIT

- $57,000 maximum annual household income in the previous year (all counties in Washington State)

HOW TO APPLY

Homeowner Improvement Exemption

WHAT IS IT?

Relief from tax increases caused by major additions or remodels.

YOU MUST…

- Own a detached single family dwelling (including mobile homes)

- File your claim for exemption with the assessor BEFORE construction is complete

HOW TO APPLY

- Call 206-263-2338

Flood & Storm Damage Property Tax Reduction

WHAT IS IT?

Tax relief for property damaged by something beyond the owner’s control. Eligible properties receive a reduction of assessed value resulting in lower property taxes. In addition, taxpayers can receive an exemption to keep taxes lower for the 3 years after they rebuild.

YOU MUST…

- Have your property on the assessment roll as of January 1st in the year it was damaged

- Have property that was destroyed, OR was in a declared disaster area and reduced in value by more than 20% as a result of the disaster

HOW TO APPLY

- Complete a Destroyed Property Claim Form and file it with King County Dept of Assessments within 3 years of the damaging event

- Call 206-263-2332 with questions

For more information on any of these programs, visit the King County Assessor’s tax relief page. You can also find info for other counties on the WA Dept of Revenue website.

Find a Home | Sell Your Home | Property Research

Neighborhoods | Market Reports | Our Team

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

2737 77th Ave SE, Mercer Island, WA 98040 | (206) 232-0446

mercerisland@windermere.com

© Copyright 2023-2025, Windermere Real Estate/Mercer Island.

The Downside of Selling Your Home Off Market

Who wouldn’t want the enticement of a full price offer on their home before it even comes to market? At first glance it seems like a compelling opportunity, but it comes at a steep price.

With the shortage of homes today, friends and neighbors are all on the lookout for up-and-coming listings. They aren’t hard to spot amongst the buzz of spruce up activity that often occurs as a home is being prepped for the market. Often the buyer or their broker contact the seller or their broker to request an early showing and you can guess what transpires from there. You and your broker have a list price in mind and the buyer’s offer comes in at that price. What could be better?

Are you leaving money on the table?

For starters, consider that homes in the Seattle-Eastside region are typically selling well above their asking prices. Local market data shows most homes bring in 3-8% above their listed prices during the last several months. This occurs when multiple buyers are competing for the same property…something that doesn’t happen when negotiating off market with a single buyer. Consider a home at Seattle’s median price of $800,000, 3-8% equates to $24,000-$64,000 left on the table.

But that isn’t all there is to consider. In our current highly competitive market, it isn’t unusual for buyers to waive contingencies such as financing and appraisal, pre-inspect or waive the inspection contingency, and often even release their earnest money as non-refundable. This does not often happen in a non-competing situation and leaves you vulnerable to transaction challenges before closing.

In addition, it is often the buyers who can’t effectively compete in an open market that are most motivated to try to get you to sell off market. This benefits the buyer significantly, but eliminates the benefits to you of a strong seller-favored market.

What about iBuyer company offers?

iBuyers are companies that agree to pay a set amount for your home up front and then list it for sale after you move out. They have gained popularity in some markets-Phoenix and Atlanta especially. In 2019, they had 59,000 transactions nationwide or about half of one percent market share of the 5.38 million transactions last year. Amidst COVID and economic concerns, iBuyer market share was down dramatically in 2020 and remains uncertain for 2021.

Nationally, their sweet spot has been predictable subdivision homes priced around $250,000. They have traditionally avoided higher priced markets due to the added risk in pricing. And they have historically avoided Washington State because of our real property transfer tax that adds ~2% to the cost of sale.

While selling to an iBuyer might seem easy and intriguing, it helps to remember these companies are in business to make a profit at your expense. iBuyers charge a 6-10% service fee in addition to factoring in the cost of needed repairs or updates (data shows an average of 2-5% of the sale price). Atypical expenses, like our state’s 2% transfer tax, are also calculated into the net. Add it all up and it is a hefty price to pay for the convenience of not having to go through the sale process.

On other thing to note is that iBuyers also profit by selling the names of homeowners who contact them for a bid, but do not accept that bid (93-98% of inquiries, depending on the company), to real estate agents without an established client base who are willing to pay for leads. These are typically not the most successful real estate brokers in a given marketplace. Not only do sellers who use these brokers often lose out on the benefits of working with a knowledgeable and established Realtor, that broker’s marketing budget is consumed largely by paying for leads instead of prominently marketing your home.

Final thoughts

It’s so easy to get caught up in the whirlwind of an off-market offer. And it’s flattering to feel like your home is so appealing that people are knocking on your door before it even debuts. For some, the privacy of an off-market sale offsets the considerable dollars left on the table. But for most of us, those dollars matter. And having multiple interested buyers instead of just one means better terms and more certainty as you head towards the closing table.

Still have questions? Contact one of our knowledgeable brokers for assistance with how to purchase, sell, or determine the value of any property you are considering.

Find a Home | Sell Your Home | Property Research | Neighborhoods | Market Reports | Our Team

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

© Copyright 2020 Windermere Mercer Island.

Waterfront Defined

Terminology

These local definitions will not only to help you know the lingo when it comes to waterfront speak, but to give you quick access tools to research waterfront to your heart’s content. Here is a quick resource to commonly used terms related to waterfront real property:

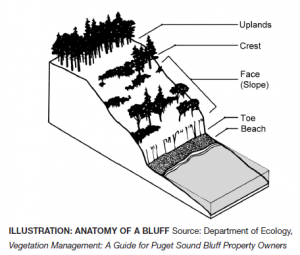

Bluff Most beaches on Puget Sound are backed by bluffs. These bluffs can vary from spectacular, high eroding cliffs to low, vegetated banks. The erosion of bluffs is a significant source of sediment on many Puget Sound beaches. One way of classifying bluffs is by the amount of sediment they provide to local beaches as they erode. This is based on how fast they erode, how high they are, and how much sand and gravel they contain. In these maps, bluffs are assigned to the following categories: Exceptional Feeder Bluffs; Feeder Bluffs; Feeder Bluff – talus; and Transport Zones. This Department of Ecology Feeder Bluffs and Coastal Landforms Map is a great tool for identifying bluff categories.

Boathouse A building designed for the storage of boats or watercraft to provide protection from the elements. The building of boathouses is generally prohibited under current environment regulations, but many grandfathered boathouses remain throughout the region.

Bulkhead A solid or open pile wall of rock, concrete, steel or timber or other materials or a combination of these materials erected generally parallel to and near the ordinary high water mark for the purpose of protecting adjacent wetlands and uplands from waves or currents.

Dock A raised walkway over water, often supported by widely spread pilings or pillars. Recent dock requirements encourage the use of decking structures and systems that encourage light and air flow to the water below. Also referred to as a pier.

Dock inspection A structural and functional evaluation by an individual or company who specializes in dock construction and repair. This can involve an underwater dive evaluation when portions of the supporting structure is in question or unobservable from above.

High bank waterfront Land that sits substantially above the natural water line, making the waterfront inaccessible without stairs or other structures, if at all.

Low bank waterfront Land that sits just above the natural water line, often delineated with a bulkhead protecting the shoreline. Low and no bank waterfront abutting a navigable lake is often considered the most desirable waterfront in the Puget Sound region.

Medium bank waterfront The most subjective of terms, this represents moderate bank land that is lower than high bank and higher than low bank waterfront.

Moorage A place where a boat or ship are secured in the water. As it pertains to waterfront real estate, this is typically on a privately owned dock or boathouse.

Navigable water “Navigability or navigable” means that a body of water is capable or susceptible of having been or being used for the transport of useful commerce. The state of Washington considers all bodies of water meandered by government surveyors as navigable unless otherwise declared by a court. See Who Owns the Water?

No bank waterfront Land that graduates out to the natural water line without a bulkhead separating it from the shoreline. Often described as rolling waterfront, its spacious feel at lakeside is highly desirable.

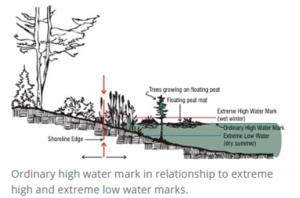

Ordinary High Water “Ordinary high water” means, for the purpose of asserting state ownership, the line of permanent upland vegetation along the shores of nontidal navigable waters. In the absence of vegetation, it is the line of mean high water.

Pier A raised walkway over water, often supported by widely spread pilings or pillars. Recent dock requirements encourage the use of decking structures and systems that encourage light and air flow to the water below. Also referred to as a dock.

Private Waterfront Land abutting the water owned exclusively by an individual land parcel. Greater waterfront footage and amenities (beach/dock/moorage) create a more valuable parcel than one with limited waterfront footage or amenities.

Shared Waterfront Land abutting the water owned in common (deeded) by owners of other often adjoining, land parcels. Fewer owner shares and deeded amenities (dock access/moorage) create a more valuable shared waterfront parcel than one with many owners or fewer amenities.

Shorelands Land which is alternately covered and left dry by the rising and falling of the water level of a lake, river, or tidal area.

“First class shorelands” means the shores of a navigable lake or river belonging to the state not subject to tidal flow, lying between the line of ordinary high water and the line of navigability, or the inner harbor line where established and within or in front of the corporate limits of any city, or within two miles thereof upon either side (RCW 79.105.060(3)). These boundary descriptions represent the general rule; however exceptions do exist. To determine if the shorelands are within two miles of the corporate limits of a city, the distance is measured along the shoreline from the intersection of the corporate limit with the shoreline.

“Second class shorelands” means the shores of a navigable lake or river belonging to the state, not subject to tidal flow, lying between the line of ordinary high water and the line of navigability, and more than two miles from the corporate limits of any city (RCW 79.105.060(17)). These boundary definitions represent the general rule; however, exceptions do exist. To determine if shorelands are more than two miles from the corporate limits of a city, the distance is measured along the shoreline from the intersection of the corporate limit with the shoreline.

(Public) Tidelands Land belonging to and held in public trust by the state for the citizens of the state, which are not devoted to or reserved for a particular use by law. Typically, the portion of land below the ordinary high water mark and the navigable water. Tide lines have been an area of great controversy in Washington State. Considered public domain through the Public Trust Doctrine. The Public Trust Doctrine does not allow the public to trespass over privately-owned uplands to access the tidelands. It does, however, protect public use of navigable water bodies below the ordinary high water mark.

“First class tidelands” means the shores of navigable tidal waters belonging to the state lying within or in front of the corporate limits of any city, or within one mile thereof upon either side and between the line of ordinary high tide and the inner harbor line; and within two miles of the corporate limits on either side and between the line of ordinary high tide and the line of extreme low tide (RCW 79.105.060(4)). In general, the line of ordinary high tide is the landward boundary. The line of extreme low tide, or the inner harbor line where established, is the waterward boundary. To determine if the tidelands are within two miles of the corporate limits of a city, the distance is measured along the shoreline from the intersection of the corporate limit with the shoreline.

“Second class tidelands” means the shores of navigable tidal waters belonging to the state, lying outside of and more than two miles from the corporate limits of any city and between the line of ordinary high tide and the line of extreme low tide (RCW 79.105.060(18)). In general, the line of ordinary high tide is the landward boundary. The line of extreme low tide is the waterward boundary. To determine if the tidelands are more than two miles from the corporate limits of a city, the distance is measured along the shoreline from the intersection of the corporate limit with the shoreline. Excerpt from the Department of Ecology Public Trust Doctrine.

Waterfront Footage The linear feet that span the water’s edge of a land parcel.

Watershed A watershed is the land area draining to a nearby river or lake, or sound.

Maps

There are many local map portals to assist in identifying topography, water conditions, hazards, and critical areas.

iMap Parcel Lookup Instructions (PDF)

Washington DNR Natural Hazards Geological Maps

Washington Geographic Information Portal Map

Department of Ecology Feeder Bluffs and Coastal Landforms Map

Department of Ecology Wetlands Inventory Map

NOAA Puget Sound Water Depth Chart

Resources

King County

King County currently has about 1200 documented residential docks and 58 private boat ramps (see shoreline land use facts). A permit is required to build, modify, alter the land abutting a shoreline.

King County Shoreline Management Fact Sheets and Links

King County Shoreline Permit Submittal Requirements (PDF)

King County Bulkhead Shoreline Requirements (PDF)

Shoreline Site Plan Requirements (PDF)

King County Shoreline Property Owner Resources

King County Lake Services and Information

Puget Sound Shoreline Stewardship Guidebook

King County Water and Shorelines Glossary

Washington State

Washington State (RCW) Aquatic Land legal definitions

DFW – Your Marine Waterfront (PDF)

DNR – Puget Sound and Coastal Geology

DNR – Puget Lowland Geological Province

Dept of Ecology – Mapping Bluffs and Beaches of Puget Sound (PDF)

WSU Guide for Shoreline Living (PDF)

UW Puget Sound Fact Book (PDF)

Environmental Protection Agency

Shoreline and Wetland Tools and Resources

King County watershed overview map

Cedar River – Lake Washington Watershed (Lake Washington waterfront properties)

Central Puget Sound Watershed (North/West Seattle waterfront on Puget Sound)

Green-Duwamish River Watershed (South Seattle waterfront properties on Puget Sound)

Sammamish Watershed (Lake Sammamish waterfront properties)

National Oceanic and Atmospheric Administration

ERMA visualization map of Puget Sound

Bluffs, landforms and habitat classifications

The Watershed Company (site evaluation contractor) Articles

A home buyer’s guide to property with critical areas

Shoreline planning and permitting

We hope this provides an outstanding starting point in your waterfront journey. In addition to this specific research, don’t forget to evaluate all the typical aspects of your potential new home and neighborhood. We’ve compiled links to research tools from schools and geological hazards to market reports and census data.

While you’re there, you can also look up neighborhood info, including crime reporting, local government resources, parks and recreation, and school boundaries.

Of course, nothing tops having an experienced broker to guide you through the process. They’ve seen hundreds upon hundreds of homes and can help you identify the solid finds from the duds with gorgeous looking veneer.

Choosing the right broker can save you thousands on your home purchase. Whether through local market knowledge and pricing analysis allowing you to make a smarter offer, recommendations and resources to thoroughly conduct your due diligence and avoid costly mistakes, or savvy contract negotiation to help you get the terms you need, having a Windermere broker on your side is one advantage you can’t afford to sacrifice.

Find a Home | Sell Your Home | Property Research | Neighborhoods | Market Reports | Our Team

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

© Copyright 2020 Windermere Mercer Island.