Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Strategic Investments to Boost Value & Curb Appeal

When it’s time to sell your home, one of the biggest questions is how to make it as appealing as possible to today’s buyers. While market conditions, location, and timing all play a role, the updates you choose before listing can make a meaningful difference in both your selling price and how quickly your home goes under contract. The key is knowing where to invest your time and money. Not every project pays off, but some smart upgrades can give your home a competitive edge, help it stand out in online listings, and create the kind of first impression that gets buyers excited.

Here are some of the most impactful ways to invest in your home before putting it on the market.

Fresh Paint and a Neutral Palette

Few improvements have a more substantial return on investment than paint. A fresh coat instantly refreshes a space, making it feel clean, updated, and well-maintained. In fact, a recent report1 by the National Association of REALTORS® found that painting is the #1 project agents recommend sellers do before selling.

Neutral tones for interiors, such as light beige, soft grays, and crisp whites, appeal to the broadest audience and allow buyers to envision their own style in the home. Check out the Sherwin-Williams Colormix Forecast 2026 for some up and coming hues (and opt for the lightest shades). It’s crucial not to overlook trim, doors, and even ceilings, as these small details help create a polished, move-in-ready feel. And if your front door could use a pop of personality, consider a bold, welcoming color that complements the rest of the exterior.

Curb Appeal That Counts

Buyers often form an impression before they even step inside. Landscaping, exterior lighting, and simple maintenance go a long way toward making your home inviting. Think trimmed hedges, fresh mulch, pressure-washed walkways, and a tidy lawn. It’s also smart to ensure outdoor areas are safe, from repairing uneven paths to addressing any obvious hazards. Here is a printable checklist so you don’t miss anything.

Adding planters with seasonal flowers, updating house numbers, or swapping out an old mailbox can elevate your home’s appearance without requiring a significant investment. For buyers scrolling through listings, that curbside charm can be a deciding factor that gets them to schedule a showing.

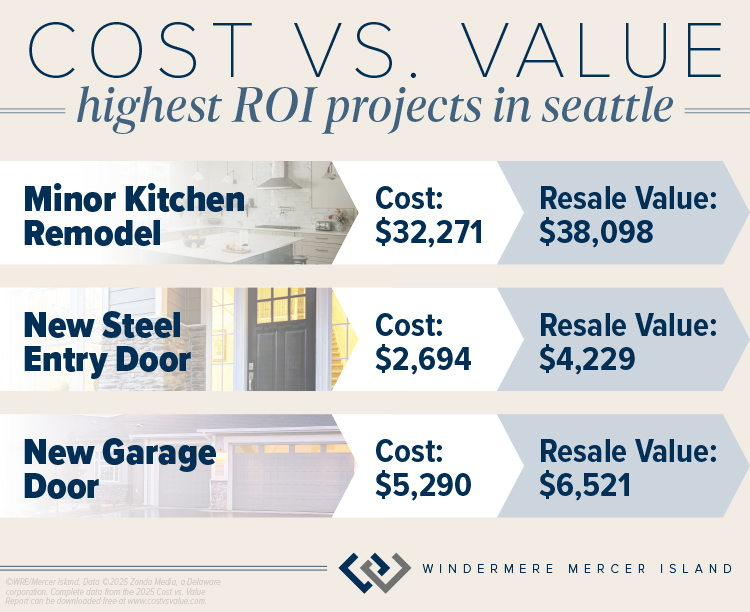

According to the latest Cost vs. Value report for Seattle2, exterior curb appeal investments such as a basic new front door or garage doors can net you a profit when it’s time to sell:

Kitchen and Bathroom Touch-Ups

Kitchens and bathrooms continue to be high priorities for buyers, but you don’t need to take on a full remodel to make an impact. Small upgrades like replacing outdated cabinet hardware, installing new light fixtures, or swapping in modern faucets can transform the look of these spaces.

In the kitchen, consider updating your backsplash with a clean, timeless tile or refreshing worn countertops with a durable surface. In bathrooms, re-grouting tile, caulking any cracks, replacing mirrors, or updating vanities are simple ways to modernize without overspending.

The Cost vs. Value report2 also found that the kitchen can be a smart place to invest in a minor remodel of surfaces and newer mid-priced appliances and fixtures. In the Seattle area, a minor remodel is estimated to recoup 118% of its cost when you sell.

Flooring Matters

Floors are often one of the first things buyers notice when touring a home. If your carpets are worn or stained, professional cleaning or even replacement can make a big difference. Hardwood floors are especially appealing and refinishing them is often more cost-effective than replacing them.

For areas where replacement makes the most sense, consider durable and stylish options like engineered wood or luxury vinyl plank. Consistent flooring throughout the main living areas can also help a home feel more spacious and cohesive.

Energy-Efficient Features

Today’s buyers are increasingly focused on efficiency and sustainability. Investments like LED lighting, programmable thermostats, and updated appliances not only lower utility bills but also signal to buyers that the home is modern and thoughtfully maintained.

If your budget allows, new windows or improved insulation can add value while appealing to environmentally conscious buyers. Highlighting these upgrades in your listing helps showcase both comfort and cost savings.

Decluttering and Staging

Sometimes the most impactful upgrade isn’t about new finishes, it’s about presentation. Decluttering each room, minimizing personal items, and rearranging furniture to optimize space can dramatically change how buyers perceive your home. Here’s a printable checklist to help. And the best part? It’s completely free.

Professional staging takes this one step further, creating a warm and welcoming atmosphere that helps buyers envision living in the space—it can also help your home sell faster and for more money according to a 2025 report3. Even small touches, like fresh flowers, cozy throws, and well-placed artwork, can make your home feel more stylish, comfortable, and truly move-in ready.

Making Smart Choices

The goal of any pre-sale investment is to spend strategically, choosing projects that increase appeal without overextending your budget. You can also refer to this article on what NOT to do.

At Windermere, our agents are experts at helping sellers decide which upgrades matter most. From recommending paint colors to connecting you with trusted contractors, we’re here to make sure you get the best return on your investment. Through our Windermere Ready program, we can even front the cost of improvements like painting, landscaping, cleaning, and staging so your home shines its brightest when it hits the market. With concierge-level service and no payments due until closing, it’s a simple way to maximize your home’s value and sell faster.

Connect with an experienced Windermere agent today to learn more about how we can help you prepare your home for the market with confidence:

Adapted from an article that originally appeared on the Windermere blog October 1, 2025.

1Copyright ©2025 “2025 Remodeling Impact Report.” NATIONAL ASSOCIATION OF REALTORS®. All rights reserved. April 9, 2025, https://www.nar.realtor/sites/default/files/2025-04/2025-remodeling-impact-report_04-09-2025.pdf.

2©2025 Zonda Media, a Delaware corporation. Complete data from the 2025 Cost vs. Value Report can be downloaded free at www.costvsvalue.com.

Find a Home | Sell Your Home | Property Research

Neighborhoods | Market Reports | Our Team

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

2737 77th Ave SE, Mercer Island, WA 98040 | (206) 232-0446

mercerisland@windermere.com

© Copyright 2026, Windermere Real Estate/Mercer Island.

A Consumer’s Guide to Homeowners Insurance

If you’re a homeowner or looking to buy a home, insuring your property is critical to protecting your investment—and if you’re getting a mortgage, it’s a must. It can be daunting trying to navigate the many options available to you. What does your policy cover…and what isn’t covered? What does the insurance company provide if your property is damaged or destroyed? Recently, the National Association of REALTORS® released this helpful guide on understanding the ins and outs of homeowners insurance. Here is a quick rundown of what you need to know…

How does property insurance work?

For certain unexpected events that cause a loss to your home or property, homeowner’s insurance can cover the cost to repair/rebuild the property and other structures like fences or garages. Most policies also cover personal belongings within the home, legal/medical fees for accidents occurring on the property, and temporary housing if a covered event (like a house fire) makes your home uninhabitable.

What losses are covered?

Your insurance policy will list the specific “perils” that are covered. The most common type of policy covers both the structure and personal assets for losses from house fires, storms, freezing, theft, vandalism, and sudden plumbing bursts—this is known as a HO-3 or “Special Form” policy. Most policies don’t cover earthquakes or natural floods (although you can get additional policies for those perils).

Is insurance required?

There are no laws requiring you to maintain homeowners insurance. However, most lenders require it for the duration of your mortgage. Required or not, it’s generally a good idea to protect your assets (especially if you have a lot of equity in your home).

What is the cost, and how is it paid?

As with many costs, insurance premiums are on the rise throughout the country (here’s how much, where, and why). Your individual policy’s cost will be based on your home’s age, size, condition, location, and other factors like whether you have a security system or have added on additional coverage. You may have the option to pay the premium annually or break it into smaller payments. If you have a mortgage, the lender usually collects a monthly “escrow” payment that they keep in an account to pay the insurance premiums and property taxes from on your behalf.

What happens in the event of a loss?

Most insurers will cover “replacement cost”—the amount needed to buy a new, comparable version of what you lost up to a dollar limit specified in the policy. It’s important to understand that replacement cost is not the same as market value; you’ll be compensated for the actual cost to repair/rebuild/replace your home regardless of what you paid for it or what you could sell it for. Typically the insurer will reimburse you to have your home repaired or replaced with comparable quality if it’s insured to at least 80% of it’s replacement cost, less any deductible that your policy has.

Alternatively, “actual cash value” is the current value of an item that depreciates over time or with use (often used for replacing personal or under-insured property). For example, if you paid $2,000 for your new couch but now it’s only worth $1,000 due to normal wear and tear, your insurer will only pay $1,000 less the deductible. You may choose to upgrade your personal property coverage to replacement cost instead for an extra fee.

For extra peace of mind, you can also purchase an extended replacement cost policy that provides extra coverage up to a set percentage above the policy limit. This can protect you if your home costs more than anticipated to rebuild.

Are the premiums tax deductible?

The short answer is no, unless you run a business from your home or it’s a rental property. However, you may be able to claim a casualty loss deduction if you suffered a loss due to a federally declared disaster (but check in with your tax pro for advice specific to your situation).

Because laws vary from state to state, it’s important to do your homework if you’re purchasing a home in an unfamiliar area. Connect with a real estate agent or your attorney for advice.

Find a Home | Sell Your Home | Property Research

Neighborhoods | Market Reports | Our Team

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

2737 77th Ave SE, Mercer Island, WA 98040 | (206) 232-0446

mercerisland@windermere.com

© Copyright 2025, Windermere Real Estate/Mercer Island.

Planning for the Life Expectancy of Your Home

Nothing in life lasts forever – and the same can be said for your home. From the roof to the furnace, every component of your home has a lifespan, so it’s a good idea to know approximately how many years of service you can expect from them. This information can help when buying or selling your home, budgeting for improvements, and deciding between repairing or replacing when problems arise.

According to a National Association of Home Builders (NAHB) study, the average life expectancy of some home components has decreased over the past few decades. (This might explain why you’re on your third washing machine while Grandma still has the same indestructible model you remember from childhood.) But the good news is the lifespan of many other items has actually increased in recent years.

Here’s a look at the average life spans of some common home components (courtesy of NAHB).

APPLIANCES. Of all home components, appliances have the widest variation in life spans. These are averages for all brands and models and may represent the point which replacing is more cost-effective than repairing. Among major appliances, gas ranges have the longest life expectancy, at about 15 years. Electric ranges, standard-size refrigerators, and clothes dryers last about 13 years, while garbage disposals grind away for about 10 years. Dishwashers, microwave ovens, and mini-refrigerators can all be expected to last about nine years. For furnaces, expect a lifespan of about 15 years for electric, 18 for gas, and 20 for oil-burning models. Central air-conditioning systems generally beat the heat for 10 to 15 years.

KITCHEN & BATH. Countertops of wood, tile, and natural stone will last a lifetime, while cultured marble will last about 20 years. The lifespan of laminate countertops depends greatly on the use and can be 20 years or longer. Kitchen faucets generally last about 15 years. An enamel-coated steel sink will last five to 10 years; stainless will last at least 30 years; and slate, granite, soapstone, and copper should endure 100 years or longer. Toilets, on average, can serve at least 50 years (parts such as the wax ring, flush assembly, and seat will likely need replacing), and bathroom faucets tend to last about 20 years.

FLOORING. Natural flooring materials provide longevity as well as beauty: Wood, marble, slate, and granite should all last 100 years or longer, and tile, 74 to 100 years. Laminate products will survive 15 to 25 years, linoleum about 25 years, and vinyl should endure for about 50 years. Carpet will last eight to 10 years on average, depending on use and maintenance.

SIDING, ROOFING, WINDOWS & DECKS. Brick siding normally lasts 100 years or longer, aluminum siding about 80 years, and stucco about 25 years. The lifespan of wood siding varies dramatically – anywhere from 10 to 100 years – depending on the climate and level of maintenance. For roofs, slate or tile will last about 50 years, wood shingles can endure 25 to 30 years, the metal will last about 25 years, and asphalts got you covered for about 20 years. Unclad wood windows will last 30 years or longer, aluminum will last 15 to 20 years, and vinyl windows should keep their seals for 15 to 20 years. Cedar decks average 15-25 years if properly cleaned and treated, while high quality composite decks should easily last 30 years with minimal maintenance.

Of course, none of these averages matter if you have a roof that was improperly installed or a dishwasher that was a lemon right off the assembly line. In these cases, early replacement may be the best choice. Conversely, many household components will last longer than you need them to, as we often replace fully functional items for cosmetic reasons, out of a desire for more modern features, or as a part of a quest to be more energy efficient.

Are extended warranties warranted?

Extended warranties, also known as service contracts or service agreements, are sold for all types of household items, from appliances to electronics. They cover service calls and repairs for a specified time beyond the manufacturer’s standard warranty. Essentially, warranty providers (manufacturers, retailers, and outside companies) are betting that a product will be problem-free in the first years of operation, while the consumer who purchases a warranty is betting against reliability.

Warranty providers make a lot of money on extended warranties, and Consumers Union, which publishes Consumer Reports, advises against purchasing them. You will have to consider whether the cost is worth it to you; for some, it brings a much-needed peace of mind when making such a large purchase. Also, consider if it the cost outweighs the value of the item; in some cases, it may be less expensive to just replace a broken appliance than pay for insurance or a warranty.

Find a Home | Sell Your Home | Property Research | Neighborhoods | Market Reports | Our Team

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

© Copyright 2019 Windermere Mercer Island.